College students who rely on student loans to pay for their education will often find themselves with several, if not a dozen or more, separate loans upon graduation.

The complication of managing multiple loans has made loan consolidation an appealing service to many cash-strapped graduates. However, like many things involving finances, deciding whether consolidation is right for you and determining how to go about it can seem complicated on the surface.

This guide explains how to consolidate your student loans online. As we explore the process, you will learn about the benefits and guidelines for determining if consolidating your loans is right for your financial situation.

What is student loan consolidation?

Student loan consolidation is where you take two or more of your unpaid student loans and combine them into one. This option is most appealing to the student who has become buried in multiple loan payments that have become due.

When you consolidate your student loans, this means that a lending institution pays off your loans for you and replaces them with a new single loan. Now, instead of making multiple monthly payments to each of your lenders, you would make a single monthly payment to your new lending institution.

What are the benefits of student loan consolidation?

The primary benefit of consolidating is that it frees up more cash for other expenses. What often happens is that graduates will be stuck with so many different loan payments, that they can’t even afford to make all of the minimum payments without sacrificing on the necessary expenses of independent living such as rent, food, and utilities.

The timing is often unfortunate for the recent graduates: they must make the most payments when they are just starting their careers and probably have the lowest income they will ever have in their lives. For many, consolidating their loans can be an effective way to get the breathing room they need while they figure out how to raise their income and manage their finances.

How do I know if consolidation is right for me?

Generally speaking, it is wise to use about 20% of your income to pay off your long-term debts no matter what your income level. This insures that you will not be burdened by debt for too long yet leaves enough income to live on without having to make unreasonable sacrifices.

You can use this “20% Rule” as a guideline. Sometimes, by having multiple loans, you will be forced to pay more than 20% of your income towards your debts because of the sum of all the minimum payments and because of the fact that you have a relatively low income because you are just starting out in your career.

However, simplifying doesn’t guarantee savings. If your only reason for consolidating is because you have a hard time keeping track of all the payments you may want to consider using auto-debit and using a service like Personal Capital to track all of your debt in a single location.

The goal of consolidation should be to reduce the monthly payment requirements by eliminating the need for multiple minimum payments. Do the math. If the numbers work then it may be a good option for you.

What if I have a poor credit score?

If you have a “fair” or “poor” credit score you may want to focus on improving your credit score before you try to consolidate your loan. You will likely not be able to get a good interest rate or even a loan at all. If you have a poor credit score and can’t afford to make your payments, applying for forbearance on your federal loans may be a better option for you. You can use the extended grace period to save some money and get a better paying job.

Understanding Your Student Loans

You likely have multiple student loans. To make matters more complicated, you might even have several types of loans. Each type of loan has it’s own rules. Here’s the basic of what you need to know:

Federal Loans

This type of loan is funded with government money. Typically, they come with low interest rates and flexible repayment options. These loans do not require any collateral or credit check, making them very popular with students. Federal student loans come in one of three forms:

- Stafford Loans (subsidized and unsubsidized)

- Perkins Loans

- PLUS Loans

Private Loans

These loans are provided by private lenders and do not use government funding. Students usually turn to these loans if the financial aid offered through their school was not enough to cover tuition. The interest rate on these loans is determined by your credit score and will typically be higher than federal loans but lower than credit card interest. In all likelihood, any loan you have that is not a Stafford, Perkins, or PLUS is a private loan.

Choosing Federal vs. Private Consolidation

You have two basic options for combining your student loans: federal consolidation or consolidating into a private loan (refinancing).

Federal Consolidation

This option is available only for federal loans (e.g. Perkins, Stafford). The government combines your separate loans into a single loan and your new interest rate is a weighted average of your previous rates.

Federal consolidations offers two key advantages:

- Income-driven repayment plans – if your monthly student loan payment is more than 10% of your income you can lower your payments by providing proof of your income.

- Public service loan forgiveness – if you consolidate your direct loans (e.g. Stafford and Perkins) you can have your remaining loan balances dissolved after 10 years in a public service job.

However, there are a couple of drawback you need to be aware of:

- Longer loan repayment schedule – while you can get your monthly payments reduced based on your income, this means that you may need to add additional years to your repayment plan because of all the extra interest you will be paying.

- Loss of Perkins loan forgiveness – The Perkins loan has its own loan cancellation programs for teachers and other public service employees. You may lose these benefits if you consolidate your Perkins loan into other loans. Read the requirements carefully and make a decision that is best-suited for your plans.

Private Refinancing

Refinancing offers you a new interest rate based on your financial condition. If you have a good credit score and a steady income you could combine all your loans and get a lower interest rate. You can consolidate both your federal and private loans through a private loan consolidation firm.

Of course, the drawback of using a private loan consolidation firm is that you will forfeit the protections you had with your federal loans such as forbearance and loan forgiveness programs. Also, you will need a good credit score to benefit from a private loan refinance.

Deciding on a Repayment Plan

The simplest way to pay off your debts is to allocate 20% of your income towards debt payments. Calculate what that number is and pay that every month by using auto-debit. If your income increases then you increase your monthly payments accordingly. This plan will insure that you pay off your debts in a timely manner yet still have enough income leftover where you won’t have to make unreasonable sacrifices.

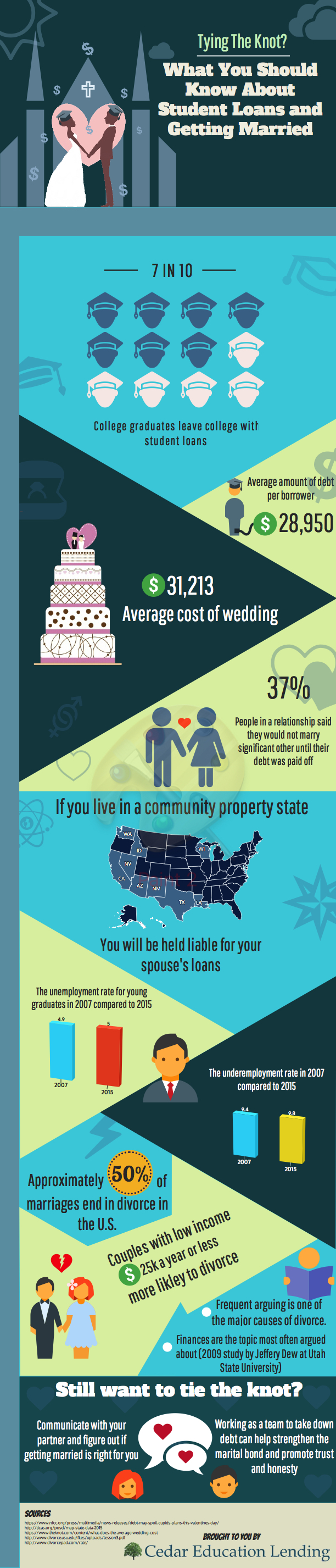

Bundling Your Loans With Your Spouse’s Loans

Many debt-ridden graduates find themselves in a position where they are married to a spouse who has student loans as well. It is possible to consolidate both persons loan into a single loan. Just don’t take this decision lightly. If you should ever divorce your spouse you will be responsible for the entire loan if the other is unable to pay. If you are going to consolidate your loans together you need to be intensely committed to staying married through life’s ups and downs and never divorcing.

Gathering the Needed Information

Once you’ve decided to consolidate your loan, you need to gather all the essential info. You will typically be required to complete the application in one sitting so you don’t want to be shuffling around trying to find the information during the application.

You should have the following items ready:

- Loan servicer names, addresses, and phone numbers

- Loan types (e.g. Stafford, Perkins, PLUS, etc.

- Account numbers

- Balances

- Federal Student ID

- Personal information: driver’s license, address, phone number, email address

- Employer’s name, address, and phone number

- Two references (full names, addresses, phone numbers, and relationships to you)

- Your last 2 paystubs

The actual application requirements may vary slightly depending on the institution and your financial circumstance, but it’s best to be over prepared than trying to scramble to find the right document before you run out of time.

Applying for a Consolidation Loan

If you’d like to apply for a federal loan consolidation, you can do that at StudentLoans.gov. If you’d like to apply for a private loan consolidation you can take advantage of Cedar Education Lending’s consolidation application. We work with a lot of different lenders to provide the best rates and repayment options available.