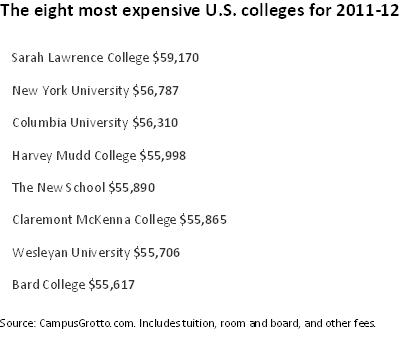

Average annual tuition at four-year private colleges for the 2011-2012 academic year is $28,500, up 4.5% from a year earlier, according to the College Board, a New York-based nonprofit that administers college entrance exams, while average room and board charges have risen 3.9% to $10,089. Between 2001 and 2012, tuition and fees at four-year private colleges rose at an annual average rate 2.6 percentage points greater than the consumer-price index. The priciest colleges now cost close to $60,000 a year.

Debt, too, is on the rise. Students who graduated from college in 2010 are shouldering an average $25,250 in debt, up 5% from a year earlier, according to the Project on Student Debt, a nonprofit research group.

The most important element in applying for financial aid is the Free Application for Federal Student Aid, also called the FAFSA, which determines how much in federal grants and aid a college-bound student will get. The form, which is used by all public and private universities, asks families to provide income and asset information, but doesn’t require you to report the value of your primary residence.

If you are attending a private college, families also must fill out the College Board’s CSS/Financial Aid Profile, which schools use to determine how to distribute their own aid funds.

The CSS takes into account factors that are largely ignored in the FAFSA. For example, the CSS looks closely at home values: Parents who have seen their home values tank in recent years should include the “quick sale” value of the home—which is roughly 80% of the value that the home is currently appraised at.  If that value is substantially below your outstanding mortgage, it can increase your aid package.

After you have exhausted all your Federal Loan options, you should look to supplement you tuition expenses with cheap Private Student Loans.And for those that have already graduated, you may want to consider refinancing some of your more expensive Private Student Loans with a Private Student Loan Consolidation.