Meeting that special someone is one of the most exciting experiences in life. Finally, you’ve found someone who understands you, someone who shares the same interests and passions as you.

But at some point in the relationship, finances will become an issue of concern. Many people rarely consider finances until after they’re married. This is bound to lead to trouble though, as finances are the #1 cause of conflict between married couples.

Now, you don’t need to sit down and cross every “t” and dot every “i” in regards to money before you get married. But if you sense the relationship is getting serious, there are some important questions that you will want to discuss with your significant other before you can confidently move forward towards marriage.

1. Do you have a similar philosophy when it comes to handling money?

Undoubtedly, you will have at least slightly different opinions on handling money. Your partner may be more willing to tolerate risks (or vice versa). You may be a deal hunter while they prefer specific brands, or perhaps one person has an expensive hobby.

These differences in preferences is inevitable. Part of maturing in a relationship is learning to understand the other person’s needs and wants and being willing to accommodate them.

However, while different preferences can be tolerated, what is extremely difficult to overcome is having fundamentally different philosophies on money-handling. For example, you will want to make sure that you are on the same page with the following questions:

Does your partner believe in saving/investing for the future?

If you’re religious, does your partner believe in tithing to your local church?

Is your partner willing to cut back expenses if needed to ensure your income remains higher than your expenses?

If either one of you brings debt to the relationship, do you have similar views on the best way to pay off the debt? (e.g. a fixed percentage of your income, consolidation, a debt forgiveness program, etc.)

If you can come to an agreement on these fundamental questions, then it’s just a matter of discussing definitions. What may seem like an “investment” to one person may be seen as an “expense” to the other. Or what one may be seen as being “thrifty” might be seen as “stingy” to the other.

These are not always easy issues to resolve, but if you have the same fundamental views of money-handling you can at least agree on the basic purpose of your money.

2. How is your significant other financing their current lifestyle? Do they have hidden debts?

At the point you start dating, your significant other will have a certain lifestyle that they have grown accustomed to. It is worth asking yourself how they finance their lifestyle.

For example, consider these common causes of debt to find out if your partner is living in a bubble that will pop sooner or later:

Reduced income/same expenses – A very common source of debt stems from simply not bringing in enough income to pay regular expenses. Someone might lead a modest lifestyle but may be relying on credit cards to make up the difference in their basic expenses like groceries, rent, utilities, cell phone, etc. If your significant other does not seem to be working much yet lives a “normal” lifestyle, you may want to raise this concern to find out where they are getting their income.

Gambling – This can be a serious issue and one that might be difficult to detect. There are many ways to gamble and most can be easily hidden or even seem harmless on the surface. Obviously, if you’re concerned you should just ask your partner. If you (or your friends or family) still suspect there might be a problem you will want to keep your eyes open–it will become apparent soon enough. You may want to reconsider the relationship if a gambling problem becomes evident.

Medical expenses – This is an unfortunate form of debt that many people struggle with. The good news is that medical expenses usually don’t indicate a character problem, but nevertheless debt is debt and must be dealt with accordingly. If your partner requires frequent operations or expensive medications you will want to make sure that they have a definite plan for paying off that debt and securing enough income to be able to afford the needed medical expenses.

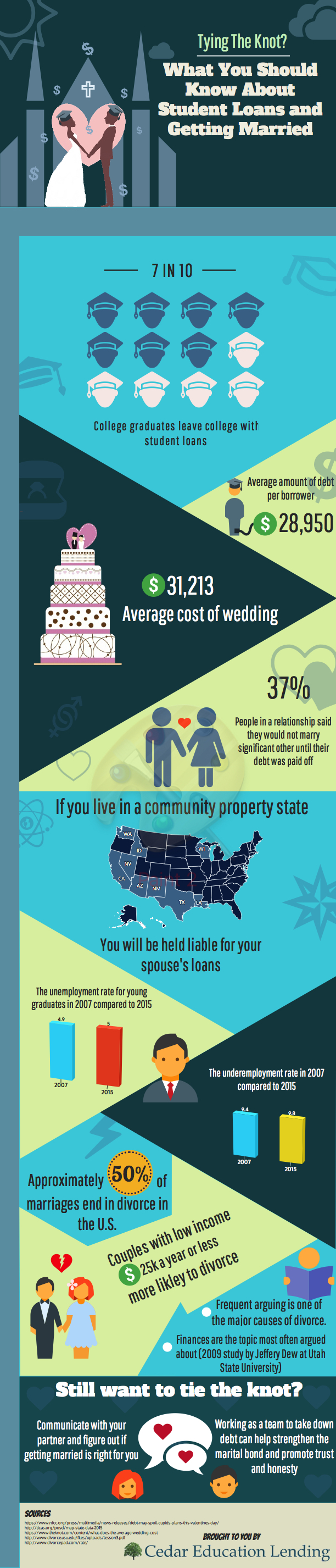

Education – A very common source of debt, especially among Millennials. Experts argue whether or not student loan debt is “worth it” but if you have it you will need to make sure that you can find a market demand for your abilities and can market yourself so you can quickly turn your experience and expertise into a reasonably high income.

Lack of savings – If your partner seems to constantly “get in trouble” financially you may need to ask them if they regularly save. You do not need to bring this up during the moment of the crisis, but perhaps after things settle down you can ask how they approach saving money. We can expect life to give us trouble from time to time and having some money set aside can give us a cushion for these “expected surprises” rather than having to get into debt every time.

3. Are they willing to undergo financial training with you?

Mastering your finances takes time and discipline so you shouldn’t expect your partner to have everything perfectly together financially. However, you do want to make sure that they are willing to learn. If they willing to learn and correct their mistakes then all of the above problems can be overcome. But if they seem to shrug off financial education as something “boring” or “stupid” then this may an early warning sign: they may never come around.

Here are a few financial training resources that many people have benefited from:

The Richest Man in Babylon – a classic book on financial wisdom written as a series of parables. It was written in 1926 and is still a bestseller today!

Dave Ramsey – a very popular financial advisor and author. Good for those who feel they need the “tough love” approach.

Ramit Sethi – very popular with Millennials. Shows you how to rely more on automation and less and willpower to make your money go where it needs to go.

4. Are they future-oriented?

Handling money requires a future-orientation of some degree. Most of the material things in life that matter most (e.g. house, education, passive income, career advancement, etc.) require thinking ahead and making plans. Very often, to obtain these things we must sacrifice some things that we might want in the moment (e.g. eating out, entertainment, hobbies, etc.).

Much of life is a balancing act between future-orientation and present-orientation. On the one hand, if we spend all our money on pleasures in the here-and-now we will still be poor and maybe even worse off when we are older. On the other hand, if you neglect the present, you may find yourself with more money but also a career that you hate, an unhappy family life, and very few real friends.

The reason you want to know if your significant other is future-oriented is because future-orientation is a result of maturity. Present-orientation is a natural childlike state (that we sometimes lose if we obsess over material success.) You want to marry someone who both enjoys life and can make good life decisions!

5. Do they let their emotions determine their financial decisions?

In a manner of speaking we usually make financial decisions based on emotions. We pay for what we value. We exchange our money for things we believe will make our lives happier.

However, it is dangerous if one is unable to check those emotional desires with logic. There will always be some shady salesman or marketer that will peddle useless products by appealing to the buyer’s emotions.

It’s perfectly fine to get excited and purchase things that will bring pleasure and betterment to our lives. We just have to be able to discern, to the best of our ability, both if something is “legit” and if it is an appropriate purchase given the present situation.

Does your significant other pass the test?

The compatibility of your financial philosophies doesn’t need to be viewed as a “pass/fail” test. Nobody’s perfect and true love and trust can overcome financial problems. But financial problems don’t go away overnight and you can expect to be in it for the long haul. So before you “tie the knot” be sure that, in addition to simply enjoying each other, there is a foundation of general agreement and transparency when it comes to finances.