The average American nuclear family needs a little extra help sending a son or daughter off to school. Surely, the wealthy family here or there can simply write up a $30,000 to $100,000 dollar check to cover the cost of the public or private colleges and universities, but the majority of people do not have such a large slush fund.

This is where student loans come in. For many students and parents, the first stop is federal financial aid, scholarships, and grants. But often these do not cover the full cost of attendance, which includes not just tuition, but boarding, meals, school supplies, and other odds-and-ends costs. When federal and state financial aid options have been exhausted and they’re often exhausted before you can cover all of your bases, you should consider private loans as a way to bridge the gap. Some students may even choose to apply for private loans to cover the entire cost of attendance, the option is there.

Private student loans are more lenient in their requirements than federal loans. Usually, all you’ll need is a letter of acceptance from a college or university or an unofficial transcript. Conversely, with the required Federal Application for Federal Student Aid as part of the federal loan process, you’ll need to supply a lot of additional information about yourself and your family.

For young students trying to navigate finance planning, the option for private loan cosigners is attractive. A cosigner is essentially somebody, usually a parent, who acts as a safety net for both you and the private loan company by promising to ensure that if the student cannot make payments themselves, the cosigner will. Also, if your cosigner has stellar credit, this may mean a better interest rate for you. (Cosigners come into play often in a young persons life. For example, you want that awesome apartment in Manhattan that requires proof of an income you don’t yet have even though your job allows you to pay the rent? Your parents can cosign if they meet the income requirement.)

It’s true that you’ll probably have more flexible repayment options with federal loans, and you should always try to find grants and scholarships first because they do not require payback. Also, it is important to remember that some private loans do have deferment options (payment postponement), while others do not. Federal loans always have a deferment period of up to 36 months, or three years. If they are subsidized, they pay the interest accrued during the deferment period; if they are unsubsidized, you will be responsible for that interest. But the reality is the same for both federal and private loans: all loans must be repaid, regardless of the way, shape, or form.

Like everything else in life, use good judgment when choosing a lender for a

private student loan. You’ve done enough shopping around in your life for sports equipment; it doesn’t hurt to gather information and compare rates, terms and repayment options. The decision you make today with your private student loans are just as important as the decisions you made when choosing your school and major. Loan repayment may take decades, so you want to be sure you are with a lender you trust and that you feel is accessible and understanding of your needs.

The horror stories are out there: an unwitting student slapped with high and hidden fees and interest rates. To make sure this doesn’t happen to you, just do your homework. Really, it’s that simple. If you are prepared, then you shouldn’t have to encounter any surprises. Don’t let the excitement of undergraduate or graduate school cause you to overlook these very important realities. Going to college often marks the beginning of adulthood, and there are very real adult decisions to be made starting from the very beginning.

There are plenty of good loan options out there. Look up as much as you can online about the major loan companies, then call and ask to speak to a representative. If your questions still haven’t been answered, try to find someone to speak with in person and schedule an appointment. Don’t rush this, and take notes, those same spectacular notes that got you accepted into college in the first place.

One benefit of private student loans comes after graduation, when you find you have all of these little bills to pay.

private student loan consolidation can make things easier by having only one monthly payment with one interest rate. And, generally speaking, you’re given a six-month grace period after graduation before you have to start repayment of either a private or federal loan.

Private student loans checks are usually mailed straight to the school. Remember, private loans can also be used to cover any school-related expense. This includes rent on an apartment while you’re going to school, or weekly groceries. Things like your computer, Internet bill and cell phone bill are usually considered school-related expenses, too.

The bottom line is that there are plenty of ways to pay for an undergraduate or graduate degree. You don’t have to let money get in the way of your future, with so many options out there for you and students just like you. The most important thing is to remember that you worked hard to get accepted and you need to enjoy the experience of higher education. A handy and helpful student loan can help you do just that.

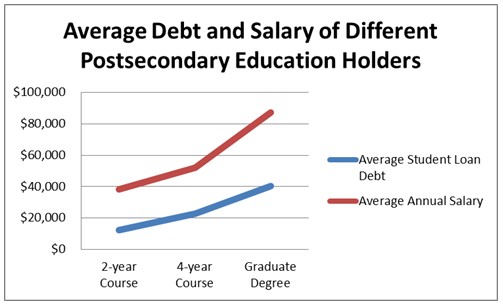

This financial quandary is amplified by the fact that non-degree holders earn significantly lower than those with a college diploma. Modern job roles, especially the high paying ones, include a Bachelor’s degree as one of the minimum qualifications. In terms of annual salary, college graduates earn an average of $52,200 versus the $30,400 of high school graduates. At this point, it’s really just simple math: the more you earn, the more money you can use to pay off debt.

This financial quandary is amplified by the fact that non-degree holders earn significantly lower than those with a college diploma. Modern job roles, especially the high paying ones, include a Bachelor’s degree as one of the minimum qualifications. In terms of annual salary, college graduates earn an average of $52,200 versus the $30,400 of high school graduates. At this point, it’s really just simple math: the more you earn, the more money you can use to pay off debt. Contrary to popular belief, today’s students are very much aware of the horror stories related to private student loans. However, many experts now agree that being scared to take out a private student loan debt can hinder the realization of a person’s full potential and can wreak greater financial havoc than staying out of debt. This is glaringly based on how much a college graduate can earn versus a non-degree holder. In a lifetime, someone with a Bachelor’s degree make $2.1 million which dwarfs the $1.2 million lifetime earnings of a high school graduate.

Contrary to popular belief, today’s students are very much aware of the horror stories related to private student loans. However, many experts now agree that being scared to take out a private student loan debt can hinder the realization of a person’s full potential and can wreak greater financial havoc than staying out of debt. This is glaringly based on how much a college graduate can earn versus a non-degree holder. In a lifetime, someone with a Bachelor’s degree make $2.1 million which dwarfs the $1.2 million lifetime earnings of a high school graduate.