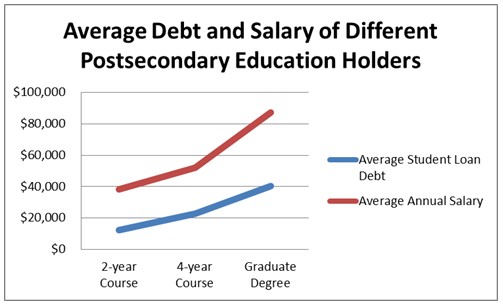

Without a doubt, student loan debt can be very overwhelming. A private student loan consolidation can make that more manageable and free up funds for other activities.

How difficult is the process? It depends on who you work with. You certainly want to work with a company that will look at your current financial situation and help you determine which private student loan consolidation program is best for you.

There are many benefits to a loan consolidation.

When you dive into a loan consolidation, a couple of things can happen:

1. You might get an interest rate reduction.

2. You may have a lower monthly payment.

These two reasons are why people decide to do private student loan consolidation. You can’t go wrong when you have less money to pay back and you don’t have such a huge monthly responsibility. It’s important to know that you can consolidate your federal education loans through private student loan consolidation. You can only combine your private loans for this type of consolidation. With Cedar Education Lending you have a private student loan consolidation program developed and managed to promote a private student loan consolidation and refinancing opportunity for college graduates with private student loan debt.

As it states on FinAid.com, since most private education loans do not compete on price, a private consolidation loans is merely replacing one or more private education loans with another. So the main benefit of such a consolidation is obtaining a single monthly payment. Also, since the consolidation resets the term of the loan, this may reduce the monthly payment (at a cost, of course, of increasing the total interest paid over the lifetime of the loan).

There are many in advantages to private student loan consolidation programs. The question is will you take advantage of them!

After highlighting the advantages of student loan consolidation, conducting a careful debt consolidation company review is essential to identify a trustworthy partner for this financial strategy. Such reviews and resources will provide insights into various companies’ reliability, customer satisfaction, and the effectiveness of debt consolidation. Understanding these aspects is vital in making the right decision that aligns with your financial goals and offers the best terms for your situation. Choosing a company with positive reviews and a strong track record can ensure a smoother consolidation process, ultimately leading to a more manageable and efficient way to tackle your student loan debt.