Undeniably, postsecondary education is one commodity that has become extremely expensive, sailing out of reach of many students. It is estimated that if the tuition and fees for college education were to be paid without any financial aid, the costs would eat up a quarter of the yearly total income of an average household.

There is no sign on the horizon that the price tag of a college diploma will go down in the next few years. It is thus natural that more students are taking out loans to finance their postsecondary education. Loan skeptics say that private student loans are traps unless you finish school and get a job. Despite the high cost, entirely foregoing your chance to get into college is more detrimental since your chances to get a good salary will be substantially reduced.

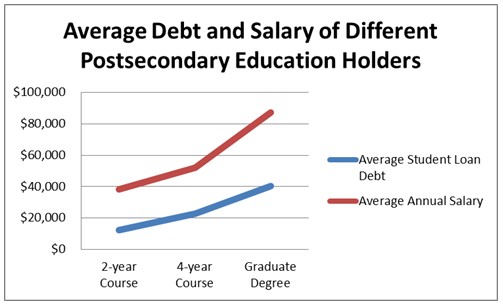

There is no sign on the horizon that the price tag of a college diploma will go down in the next few years. It is thus natural that more students are taking out loans to finance their postsecondary education. Loan skeptics say that private student loans are traps unless you finish school and get a job. Despite the high cost, entirely foregoing your chance to get into college is more detrimental since your chances to get a good salary will be substantially reduced.The average debt of those who enter postsecondary schools is approximately $47,503 dollars. This covers students of 2-year courses, 4-year Bachelor’s programs and graduate students. It is fairly usual that students borrow money from several creditors with varying interest rates and different repayment schemes. Tracking these loans can be difficult and the chance of missing a payment is high.

This is where private student loan consolidations come in handy. By collapsing all your debts into one private student loan debt, interest rates can be significantly lowered and monthly payment can be reduced to a more manageable figure, primarily by restructuring and extending your repayment schemes. Educational lending companies, such as Cedar Education Lending, offer private student loan consolidations without pre-payment penalties and interest-only payment options. You can take advantage of a 15-year repayment schedule which can ease the pressure of paying your private student loan debt.

Despite the skyrocketing costs, climbing up the education ranks is still the best way to enhance your chances at getting a financially rewarding career and life. Paying off a private student loan may seem like a big hurdle to overcome, but with the help of private student loan consolidation companies coupled with substantial financial literacy, your private student loan will be gone before you even know it.

This financial quandary is amplified by the fact that non-degree holders earn significantly lower than those with a college diploma. Modern job roles, especially the high paying ones, include a Bachelor’s degree as one of the minimum qualifications. In terms of annual salary, college graduates earn an average of $52,200 versus the $30,400 of high school graduates. At this point, it’s really just simple math: the more you earn, the more money you can use to pay off debt.

This financial quandary is amplified by the fact that non-degree holders earn significantly lower than those with a college diploma. Modern job roles, especially the high paying ones, include a Bachelor’s degree as one of the minimum qualifications. In terms of annual salary, college graduates earn an average of $52,200 versus the $30,400 of high school graduates. At this point, it’s really just simple math: the more you earn, the more money you can use to pay off debt. Contrary to popular belief, today’s students are very much aware of the horror stories related to private student loans. However, many experts now agree that being scared to take out a private student loan debt can hinder the realization of a person’s full potential and can wreak greater financial havoc than staying out of debt. This is glaringly based on how much a college graduate can earn versus a non-degree holder. In a lifetime, someone with a Bachelor’s degree make $2.1 million which dwarfs the $1.2 million lifetime earnings of a high school graduate.

Contrary to popular belief, today’s students are very much aware of the horror stories related to private student loans. However, many experts now agree that being scared to take out a private student loan debt can hinder the realization of a person’s full potential and can wreak greater financial havoc than staying out of debt. This is glaringly based on how much a college graduate can earn versus a non-degree holder. In a lifetime, someone with a Bachelor’s degree make $2.1 million which dwarfs the $1.2 million lifetime earnings of a high school graduate.